Week of February 3, 2026

(Data sourced from Altos Research, updated every Tuesday)

📊 Big Picture

This week’s data continues to reinforce a key theme across the North Shore and North Suburbs: there is no longer one market — there are many micro-markets moving at different speeds.

Mid-priced suburbs are still showing the strongest seller leverage, while upper-tier and luxury markets remain selective and deliberate. Inventory remains historically low overall, which is supporting prices, but buyers are no longer rushing. They are strategic, price-aware, and selective.

This is firmly a strategy market, not a momentum market.

📈 Suburban Trends

Mid-Priced Suburbs — Still the Most Competitive

Buffalo Grove

• MAI: 55

• Inventory: 9 homes

• Median List Price: $540K

Buffalo Grove remains a strong seller’s market. Inventory is extremely tight, and homes under $600K continue to attract quick activity when priced correctly. Even with a slight MAI pullback, buyer demand remains strong. the MAI (Market Action Index) compares the rate of sales versus inventory. A number over 30 puts the MAI in a sellers' market.

Deerfield

• MAI: 46

• Inventory: 14 homes

• Median List Price: $849K

Deerfield strengthened again this week. Rising MAI confirms improving buyer demand, while inventory remains constrained. This continues to be one of the most reliable seller-advantaged markets in the North Suburbs.

📌 Takeaway:

Buffalo Grove and Deerfield remain the most competitive environments for buyers, with sellers holding clear leverage.

Balanced Markets — Seller-Leaning but Price-Sensitive

Glenview

• MAI: 44

• Inventory: 22 homes

• Median List Price: $1.066M

Glenview remains seller-leaning, but momentum has cooled slightly. Buyer demand is still present, though pricing discipline is increasingly important, particularly above $1M.

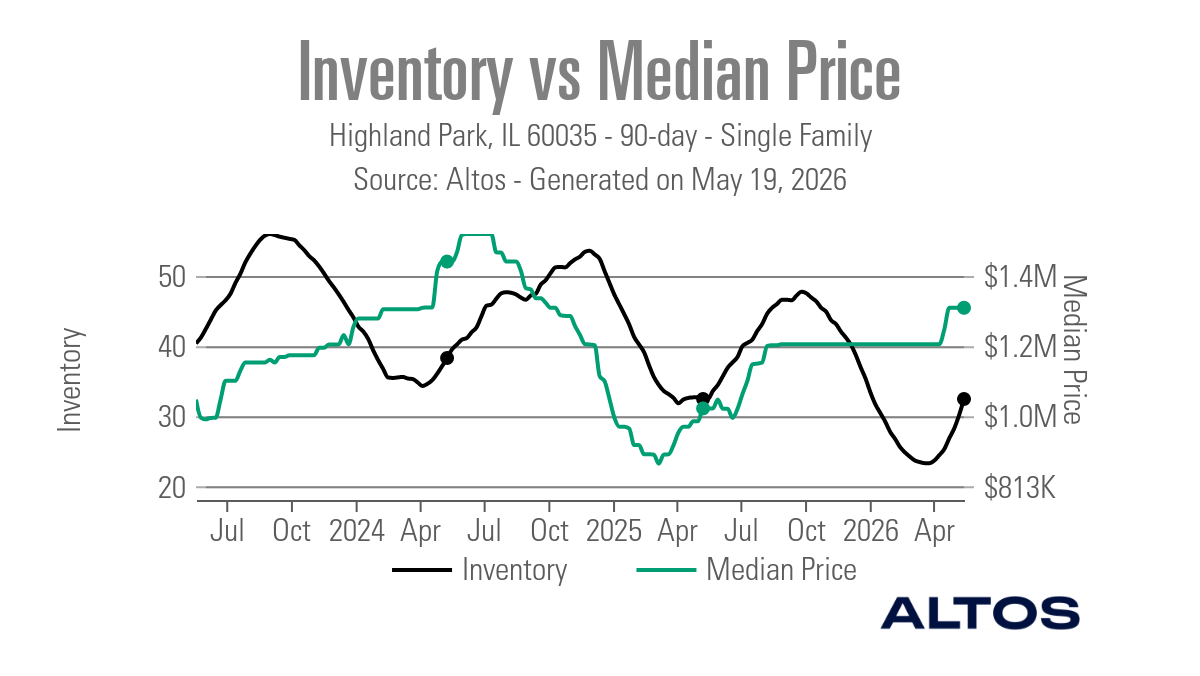

Highland Park

• MAI: 43

• Inventory: 22 homes

• Median List Price: $1.199M

Highland Park showed modest strengthening in demand this week. Inventory remains tight, but pricing has reached a plateau. Homes that are well-positioned continue to draw interest.

Northbrook

• MAI: 39

• Inventory: 23 homes

• Median List Price: $1.650M

Northbrook saw improved buyer activity paired with declining inventory. This remains a slight seller’s market, though buyers still have more leverage here than in Buffalo Grove or Deerfield.

📌 Takeaway:

These markets reward realistic pricing and strong presentation. Overpricing leads to longer days on market.

Upper-Tier & Luxury — Slow, Stable, and Selective

Glencoe

• MAI: 31

• Inventory: 13 homes

• Median List Price: $3.199M

Glencoe remains a slower-moving luxury market. Demand improved modestly this week, but buyers remain patient and highly selective. Longer days on market are still common.

Lake Forest

• MAI: 34

• Inventory: 25 homes

• Median List Price: $2.395M

Lake Forest continues to operate in a steady, seller-leaning environment. Inventory is tightening slightly, but buyers remain deliberate, particularly above $2M.

Luxury Standouts — Wilmette and Winnetka

Wilmette

• MAI: 55

• Inventory: 14 homes

• Median List Price: $2.247M

Wilmette remains a strong seller’s market, even as inventory has increased slightly. Demand remains healthy, but buyers are more selective than earlier in the year.

Winnetka

• MAI: 51

• Inventory: 11 homes

• Median List Price: $1.650M

Winnetka strengthened this week. Rising MAI and falling inventory confirm renewed buyer activity, even as prices show some softness. Despite longer days on market, this remains a seller-leaning luxury market due to extremely limited supply.

📌 Takeaway:

Wilmette and Winnetka continue to be two of the tightest luxury markets on the North Shore, with demand outpacing inventory.

💡 Key Insights This Week

• Strongest seller leverage: Buffalo Grove, Deerfield, Wilmette, Winnetka

• Most balanced conditions: Glenview, Highland Park, Northbrook

• Luxury buyers have the most leverage: Glencoe, Lake Forest

• Inventory remains historically low across nearly all suburbs

• Pricing accuracy matters more than timing

💰 Mortgage Rate Update

Mortgage rates remained relatively stable this week, with 30-year fixed rates generally ranging from the low-6% to mid-6% range, depending on credit profile and lender. Rate stability is keeping buyers engaged, but affordability remains a key factor — reinforcing the importance of strategic pricing.

🧭 Final Thoughts

This week made one thing very clear:

there is no “average” North Suburban market anymore.

Some suburbs reward speed. Others reward patience.

Understanding which market you’re in — and how buyers are behaving there — is the real advantage right now.

As always, stay informed, stay strategic, and Be Wise About the Market.