📊 Big Picture

The fall market across Chicago’s North Suburbs continues to show remarkable resilience — but it’s a story of diverging paths.

While demand remains high in the mid-priced communities (Buffalo Grove, Deerfield, Glenview), we’re seeing growing balance in the upper-tier suburbs (Highland Park, Northbrook, Glencoe, Winnetka, Wilmette).

Across the board, inventory ticked down slightly, and most towns saw either steady or climbing Market Action Index (MAI) readings — a signal that buyer activity remains strong despite seasonal slowdown.

But the real story?

We’re entering what I’d call a “strategy market” — one where pricing precision and timing make the difference between multiple offers and sitting still.

📈 Suburban Trends

Mid-Priced Suburbs — Still the Most Competitive

- Buffalo Grove: MAI jumped again to 59 from 54 last month, now the highest in the North Suburbs. Inventory dropped from 25 to 21 homes, with a median list price of $579,000. That’s a clear sign of buyers competing over limited options.

- Deerfield: MAI climbed to 47 from 44, confirming a strengthening seller’s position. Inventory fell slightly to 22 homes, and the median list price held near $753,500 — steady prices paired with firm demand suggest momentum heading into November.

- Glenview: Edged up from an MAI of 45 to 47, maintaining a solid seller’s market. Median list price rose modestly to $1.17M. Homes under $1M are still seeing the most action.

📌 Takeaway: These communities continue to perform like “micro hot markets.” Demand is sustained, inventory is tightening, and sellers who price in line with recent comps are still seeing fast activity.

Balanced Markets — Shifting, but Still Steady

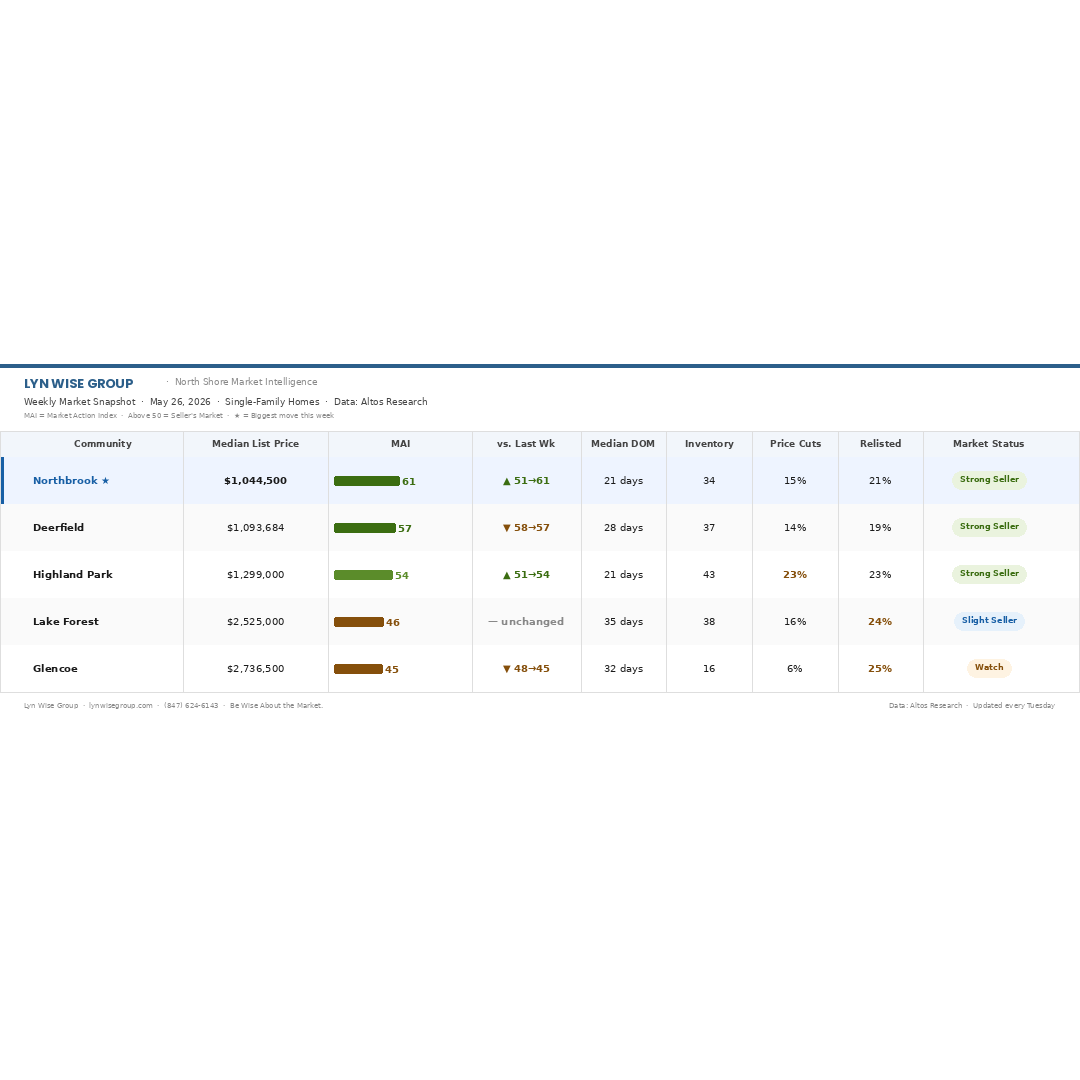

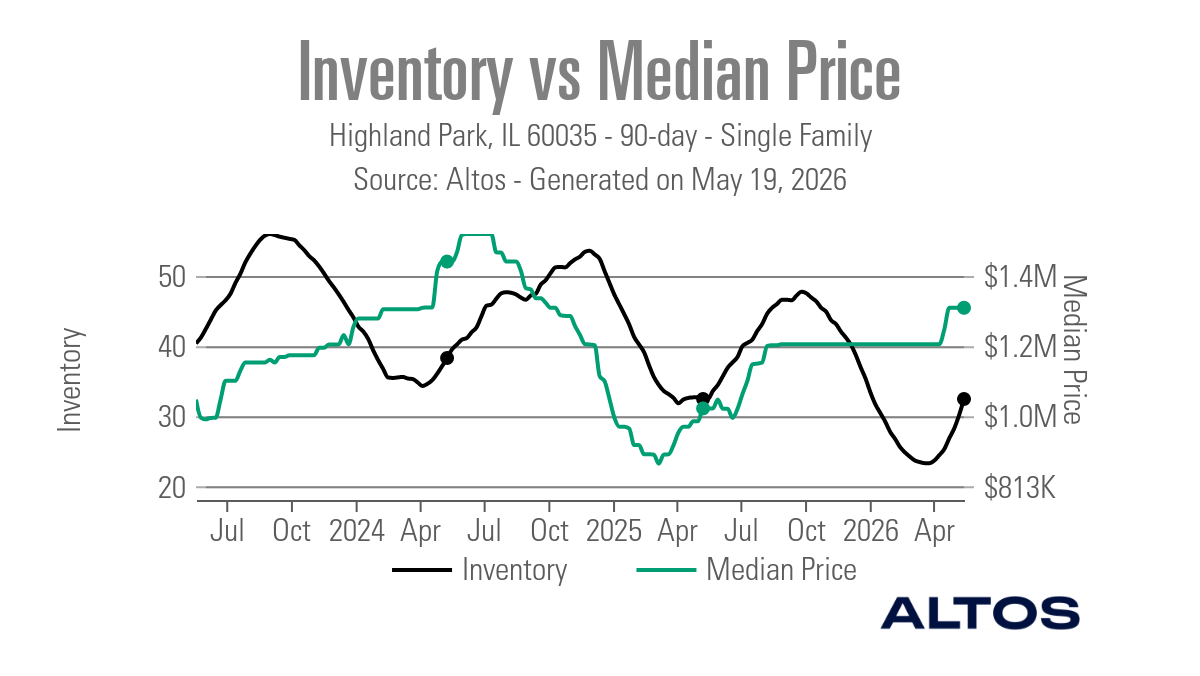

- Highland Park: Holding a 42 MAI, unchanged from last week but inventory slipped to 41 homes. Median prices remain near $1.17M, suggesting the market has found equilibrium. Expect mild activity until post-holiday buyers re-emerge.

- Northbrook: MAI eased to 36 (down from 40), indicating cooling demand. Median list price is now $1.72M with 44 active listings. Sellers still hold a slight advantage, but the tone is clearly softening.

- Glencoe: Continued to drift down, with MAI at 35 (from 38). Inventory fell to 15 homes, but that’s mostly due to seasonality — not a rush of sales. Median list price stands at $2.99M, and days on market remain long.

📌 Takeaway: These suburbs have transitioned from red-hot to rational. It’s still a seller’s market, but buyers have more breathing room — especially in listings over $1.5M.

Luxury Segment — A More Patient Market

- Wilmette: MAI rose sharply to 62 (from 54), signaling a surprising late-season surge in demand. Inventory is just 19 homes, making this one of the few luxury suburbs trending tighter right now.

- Winnetka: MAI steady at 40, with inventory up to 21 homes and a median list price of $2.5M. Activity is steady, but buyers are deliberate — high-end listings need clear value and presentation to move.

📌 Takeaway: Luxury sellers need to stay realistic. Demand exists, but buyers at $2M+ are cautious and patient. Sellers who’ve adjusted to the new pricing reality are the ones going under contract.

💡 Key Insights

- Overall Market Tone: Still seller-favored — but the gap between the most competitive and softest suburbs is widening.

- Inventory Movement: Slight seasonal decline, but not dramatic. We’re heading into November with active demand across most price points.

- Buyers: Opportunity is returning, especially in upper-tier homes where days on market exceed 90+.

- Sellers: Well-prepped listings still move fast. Overpricing is punished — fast.

🔍 This Week’s Quick Stats

|

Suburb |

MAI |

Change vs. Last Week |

Market Tone |

Median List Price |

|

Buffalo Grove |

59 |

▲ Up 5 |

Strong Seller’s |

$579K |

|

Deerfield |

47 |

▲ Up 3 |

Strong Seller’s |

$754K |

|

Glenview |

47 |

▲ Up 2 |

Strong Seller’s |

$1.17M |

|

Highland Park |

42 |

— |

Slight Seller’s |

$1.17M |

|

Northbrook |

36 |

▼ Down 4 |

Slight Seller’s |

$1.72M |

|

Glencoe |

35 |

▼ Down 3 |

Balanced |

$2.99M |

|

Wilmette |

62 |

▲ Up 8 |

Strong Seller’s |

$1.15M |

|

Winnetka |

40 |

— |

Slight Seller’s |

$2.5M |

🧭 Final Thoughts

As we move deeper into November, the North Suburbs market is healthy, selective, and strategic.

For sellers, pricing precisely for today’s market — not last spring’s — remains key. For buyers, this is your window to make strategic offers before 2026 momentum returns.

Next week’s data will tell us whether these trends are stabilizing or if the early signs of holiday slowdown are beginning to take shape.

Until then — stay informed, stay strategic, and as always, Be Wise About the Market.