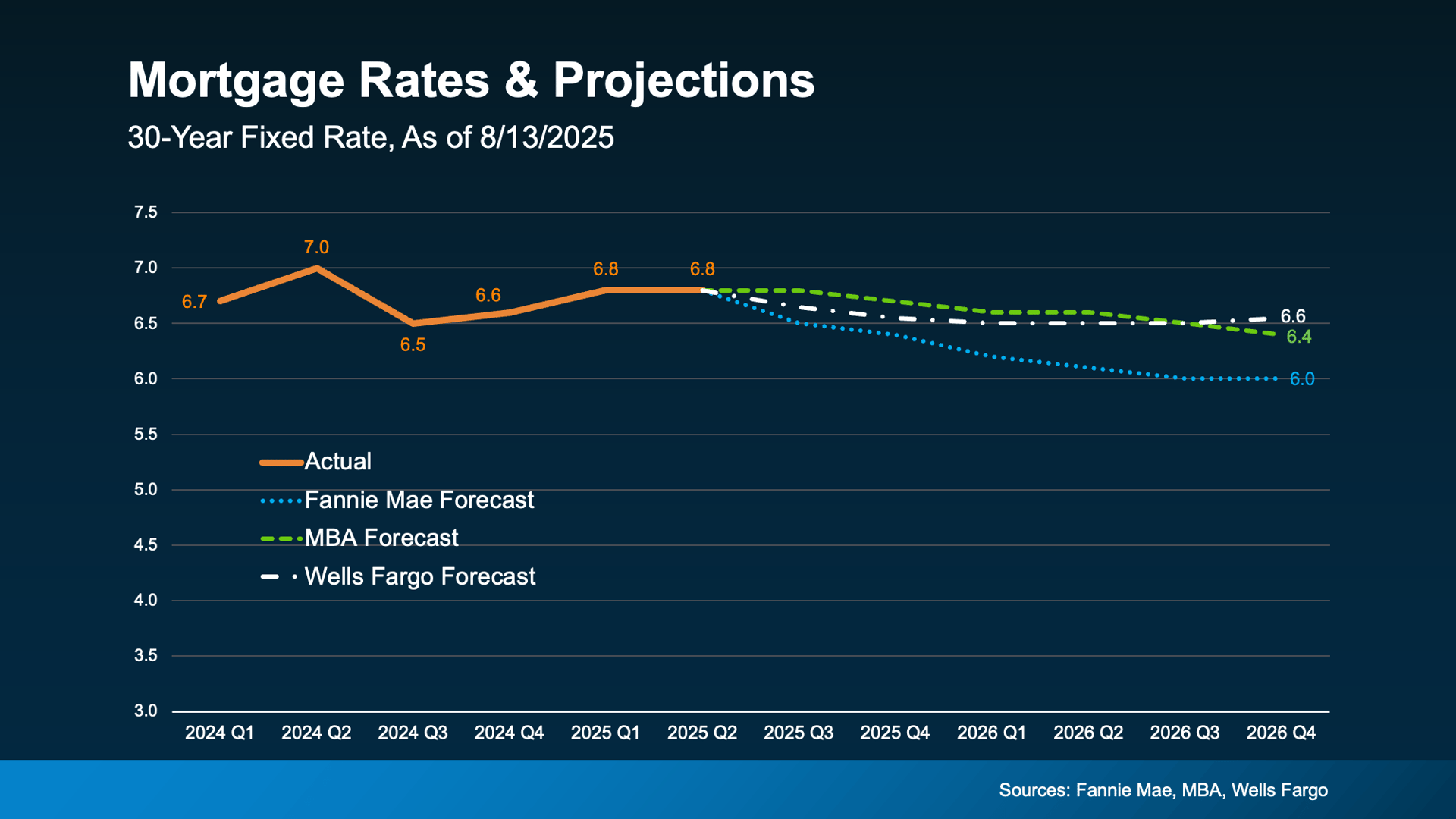

Mortgage rates continue to dominate headlines—and for good reason. Recently, a weaker-than-expected jobs report shook the bond markets, prompting a notable dip. As of early August 2025, the national average for a 30‑year fixed-rate mortgage declined to around 6.63 %, the lowest mark since April. Some sources—like Bankrate—report slightly higher figures, with the 30‑year fixed around 6.71% as of August 12, down from 6.74% the prior week; the 15‑year rate also eased to about 5.87%.

Why Buyers Monitor the 6% Threshold

That 6 percent rate is more than a psychological marker—it has real impact. The National Association of Realtors (NAR) projects that if rates hit 6%, approximately 6.2 million households would regain affordability for the median-priced home. This could ignite a jump in homebuying—up to 550,000 more buyers acting in the next 12–18 months.

So, waiting for that threshold may feel prudent. But it's important to see the flip side.

If Rates Dip, Competition Likely Increases

Delaying purchase because you're chasing lower rates can come with unintended downsides:

- More buyers re-entering the market all at once could mean higher demand, fewer listings, and bidding wars that push prices up.

- Right now, inventory is elevated compared to the recent past, giving buyers more choices.

- Price growth is slowing, and sellers are more flexible giving you greater negotiating power.

- In fact, NAR puts it plainly: buyers waiting for lower rates might let go of a valuable window to secure a better deal.

In current conditions, buyers face less competition, better pricing, and negotiation leverage—advantages that may erode once rates dip further and demand surges.

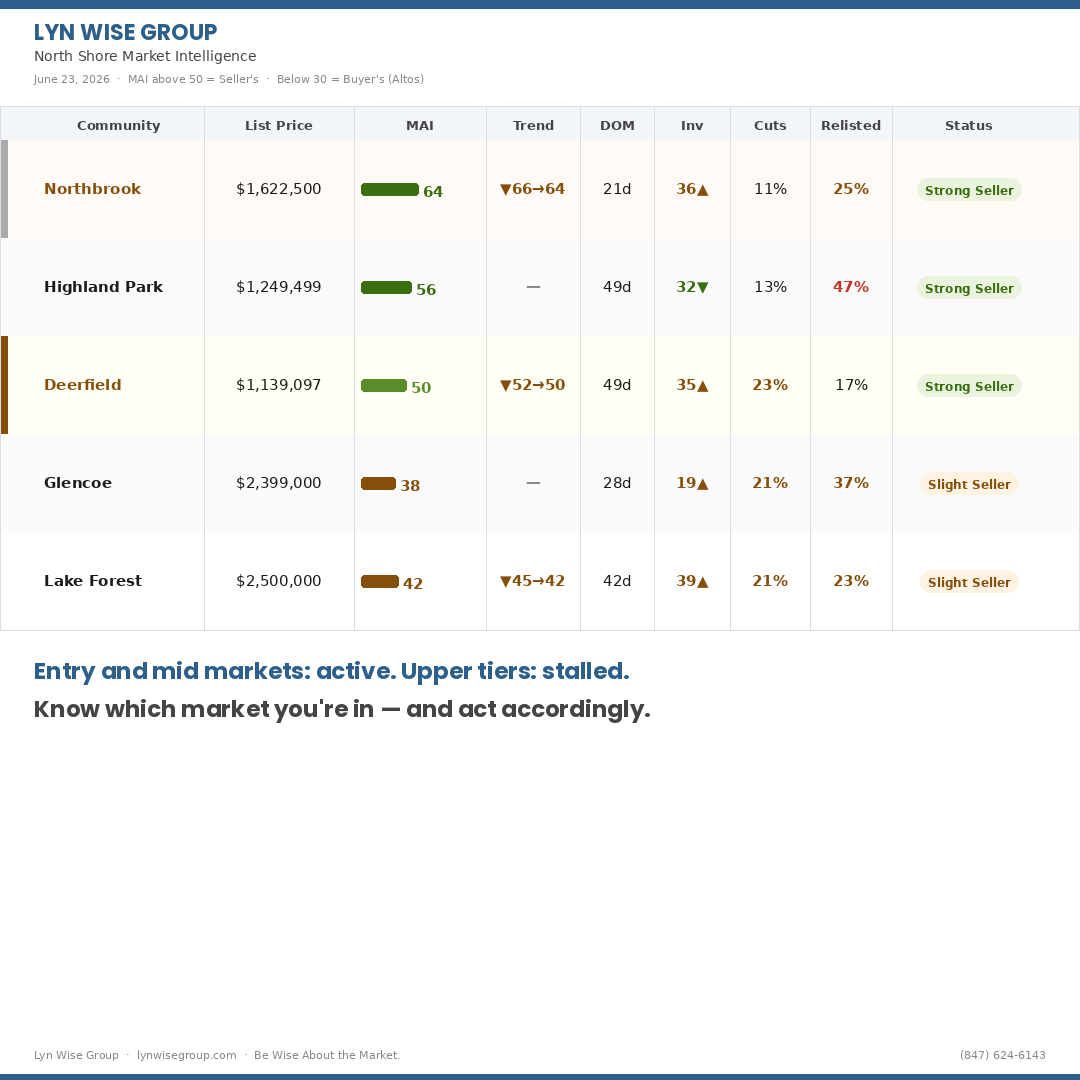

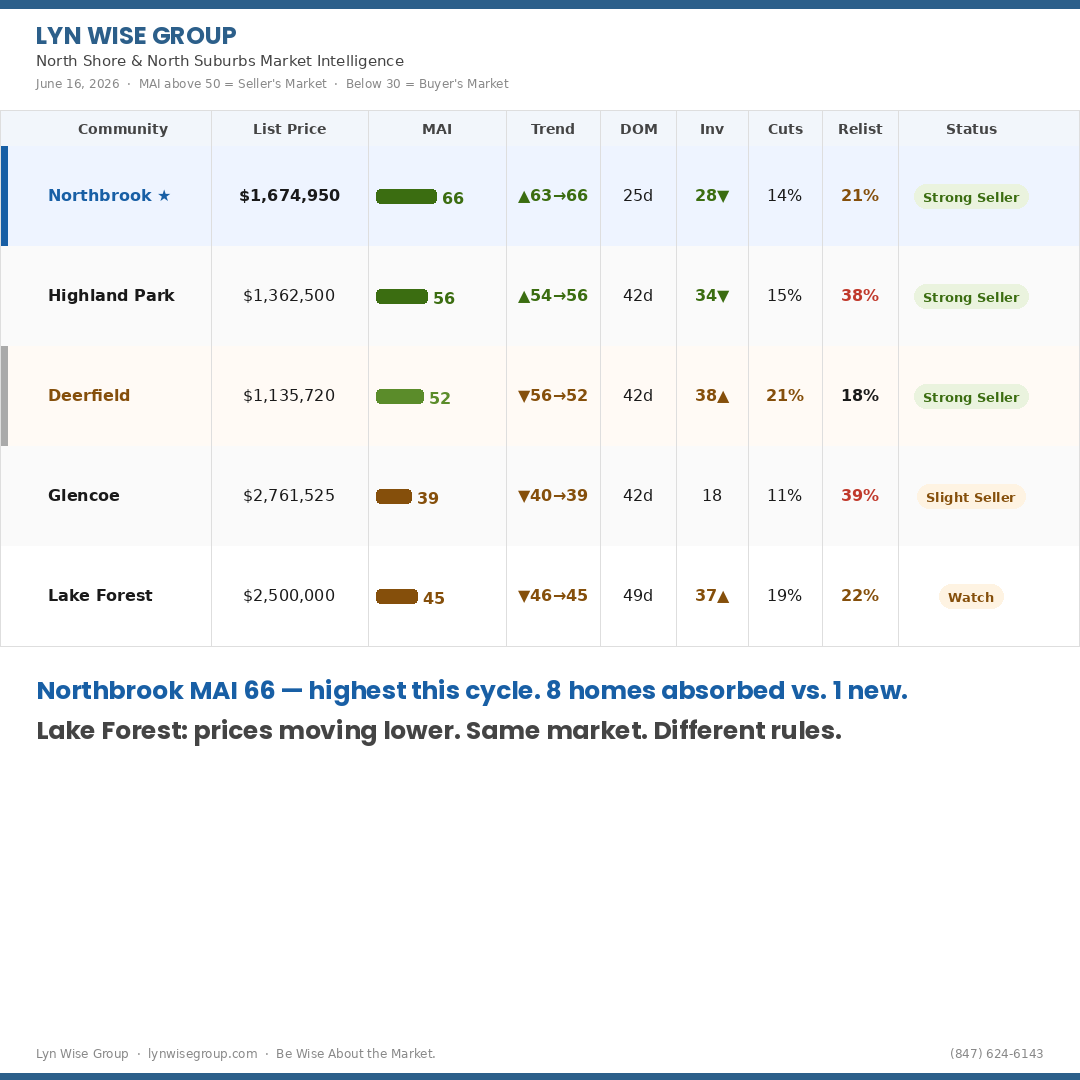

What About Here on the North Shore?

At the end of July 2025, the median listing price was about $797,000, representing a fairly significant increase year-over-year. Homes are competitive: on average, they sell in 32 days, and many receive multiple offers.

Despite cooling inventory nationwide, affordable housing, especially for first time buyers, remains a major issue locally. So, in a high-end market like Highland Park, Northbrook, Deerfield, Glencoe, Lake Forst and more, even modest shifts in affordability or demand can have outsized effects.

Bottom Line: Weighing the Trade-Off—Nationally and Locally

National Perspective:

- Rates are still high, but cooling, hovering around 6.6–6.7%, with modest declines expected.

- Rates aren’t forecasted to drop dramatically, likely staying in the mid‑6% range through 2025.

- Waiting may mean battling higher prices and competition when others jump in.

Local Insight:

- Market remains competitive, though slightly cooler than peak frenzy, and houses still sell quickly at rising prices.

- Inventory isn’t abundant, and affordable options are limited so timing can mean the difference between getting in or getting priced out.

- Now is a moment when buyers hold some negotiating room—rates have dipped, and supply isn’t yet overwhelmed.

Should You Buy Now—or Wait?

If you’re looking for less competition, more negotiating power, and a chance to lock in today’s lower rates, acting now makes sense. Waiting for rates to dip further could align you with many others doing the same—potentially increasing prices and reducing bargains.

On the other hand, if you’re not urgent, can tolerate some financial uncertainty, and believe rates may ease later waiting could pay off. But even a slight delay in our local North Shore and many other Chicago suburbs may result in a thinner pick of homes, faster competition, and fewer good deals.

Final Thought

National data shows mortgage rates dipping modestly but staying elevated, while forecasts suggest only gradual movement. Locally, buyer leverage still exists but could get squeezed once rates drop and demand rises.

In plain terms: If you’re financially ready, buying now gives you breathing room including more options, negotiating leverage, and some buyers’ control. If you wait for slightly lower rates, be ready for tougher competition and fewer opportunities. Let’s chat about how that aligns with your goals, timeline, and the unique dynamics of our North Shore market.