Overview of the Situation

On August 25–26, 2025, President Trump announced he was firing Federal Reserve Governor Lisa Cook, citing alleged mortgage fraud. Cook has refused to resign, arguing he lacks legal authority to remove her without cause. A drawn-out legal battle now seems likely.

The move rattled markets. Short‑term Treasury yields dropped while 30‑year yields, the benchmark most tied to mortgage rates, rose to about 4.92%, widening the yield curve. Analysts worry long-term inflation expectations and institutional instability could outweigh any short-term political maneuvering.

Some believe that if President Trump succeeds in reshaping the Fed board, he might pressure for rate cuts. But others say interference may backfire, leading markets to demand higher yields, especially on long-term instruments like mortgages.

President Trump has also repeatedly expressed dissatisfaction with Jerome Powell, Chair of the Federal Reserve, over the fact that he has kept interest rates high and has not made the necessary moves towards reductions. Trump has indicated his willingness to replace Powell on several occasions.

Fed Chair Powell recently hinted at an upcoming rate cut, partly due to slowing employment, not political pressure. That encouraged a recent drop in mortgage rates, showing how effective data‑driven policy can align market expectations.

What Actually Drives Mortgage Rates

- Direct vs. indirect control: The Fed sets short-term interest rates, but it's bond markets, and especially 10-year Treasury yields, that largely determine long-term borrowing costs, such as 30-year mortgage rates.

- Inflation tensions: Inflation concerns are another key factor mortgage rates incorporate.

- Mortgage rates tend to respond best to signals that cuts are justified by economic data, not politics. Powell’s recent remarks, indicating easing due to a softening labor market, have already helped lower mortgage rates.

What This Means for First-Time Buyers

If you're a first-time buyer wondering whether mortgage rates are about to drop sharply, here's the reality check:

- The Fed doesn’t control mortgage rates directly. While rate cuts can influence borrowing costs, the bond market (especially the 10-year Treasury) drives mortgage rates.

- Waiting for politics to "fix" affordability may backfire. Hoping that political moves lead to cheaper mortgages may be wishful thinking. Instead, look at fundamentals: If rates dip due to softer economic data (like slowing job growth), you’ll want to be ready to act.

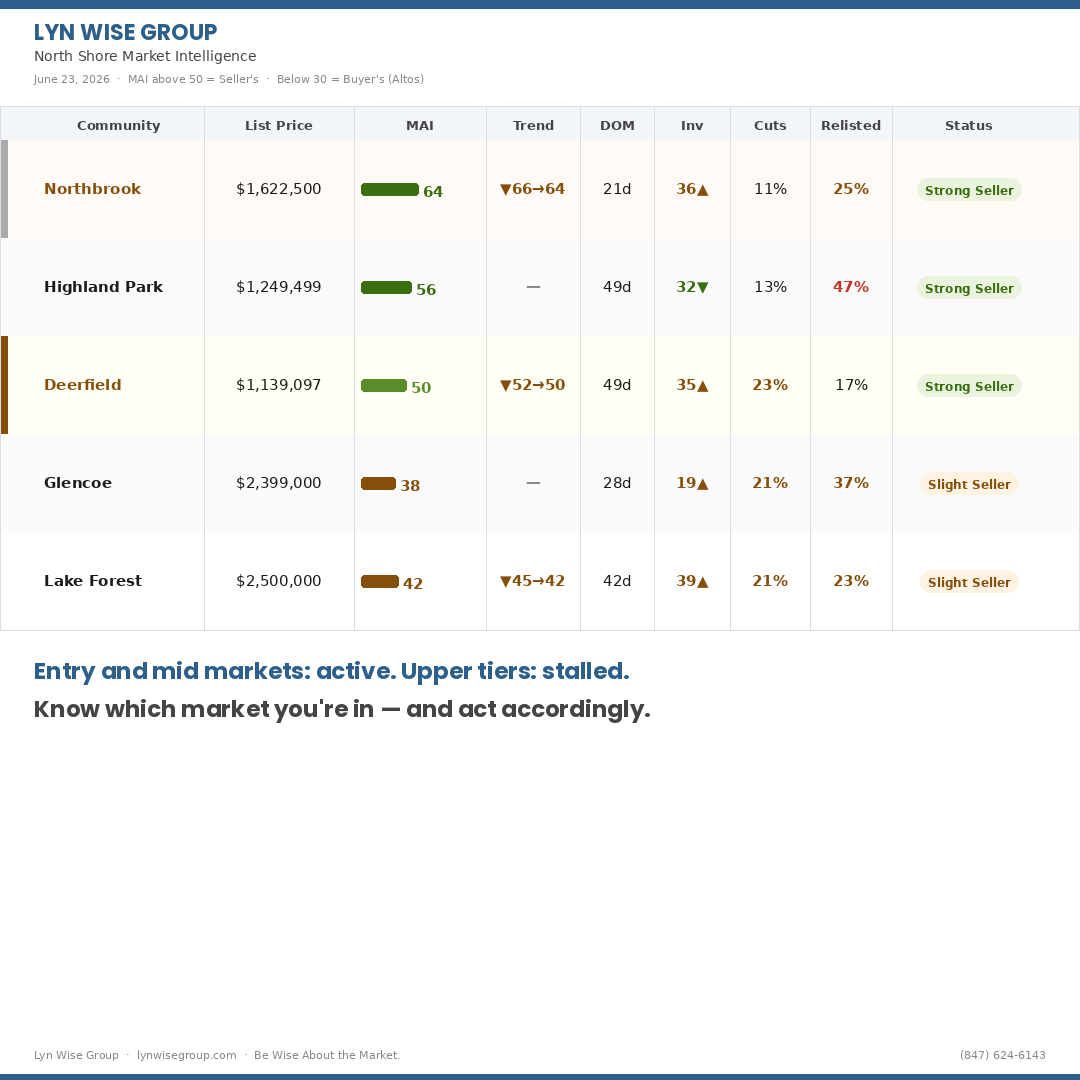

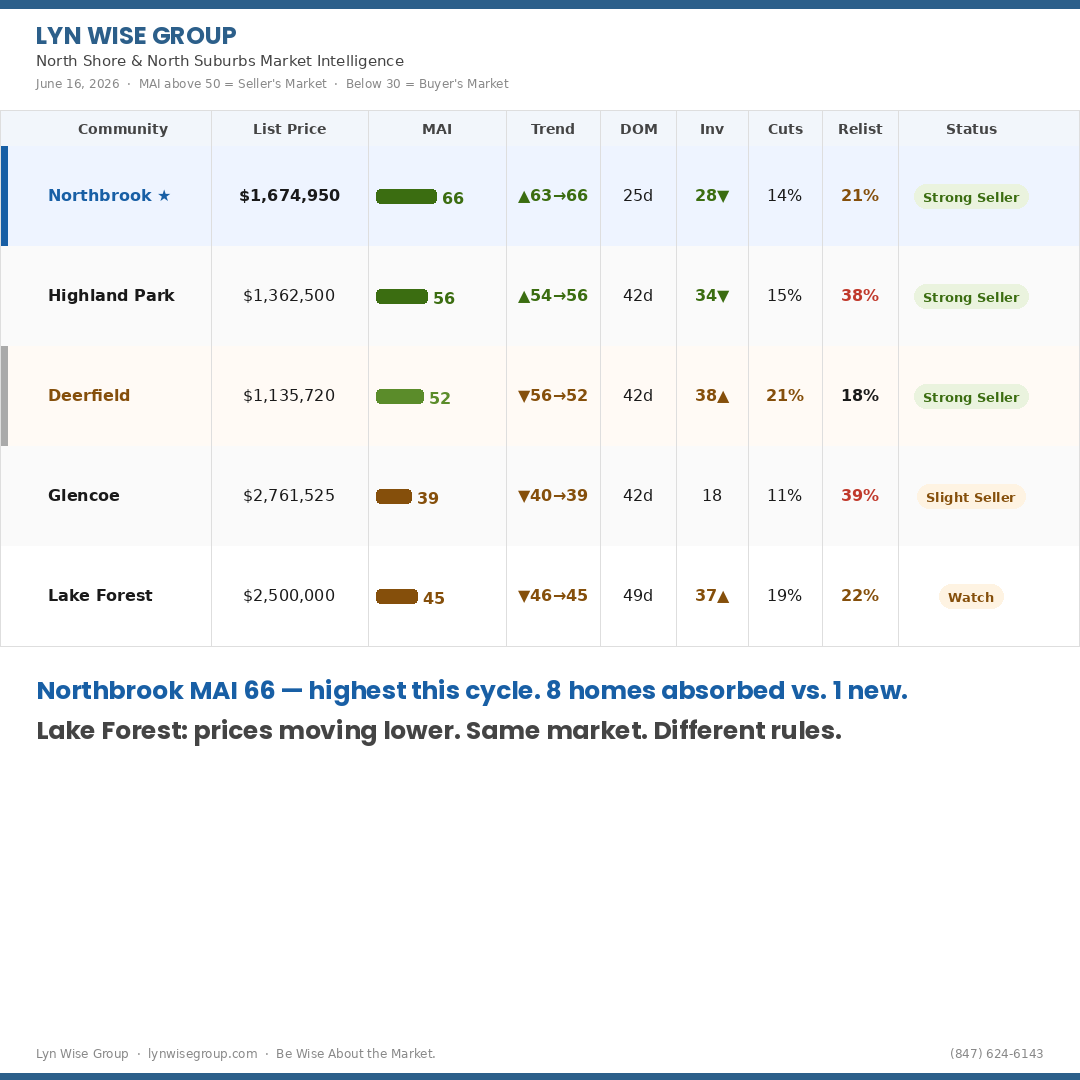

In July–August 2025, months of inventory remained below 2.0 months in Highland Park for homes under $850K — a strong seller's market. Buyers waiting for that "perfect" 5.5% rate may find themselves priced out due to bidding wars when it finally arrives.

- There may be a sweet spot soon. With home prices stabilizing in some areas and early signs of rate relief, being pre-approved and educated now puts you in position to move when the time is right.

What This Means for Downsizers & Empty Nesters

If you’re a downsizer or empty nester, thinking about selling your larger home and buying something more manageable, this latest political drama may feel like yet another reason to wait. But here’s what you should consider:

- Selling in a strong market: In many parts of Chicago’s North Shore, we’re still seeing low inventory and fast-moving listings in the $900K–$1.5M range, prime for move-up and move-down buyers. If you wait for rates to drop just right, you may miss the pricing window on your current home. In Highland Park, homes between $1M–$1.5M are still moving quickly, averaging 15–20 days on market, especially if priced right. This creates a strong launchpad to downsize with maximum proceeds.

- Buying into a shifting market: If mortgage rates stay elevated, your next purchase (townhome, condo, or ranch-style home) may cost more monthly, even if prices are flat. But if rates ease due to economic factors, inventory competition could rise sharply.

Townhomes and ranches priced between $550K–$900K in Highland Park, Northbrook and Deerfield are seeing increased interest from downsizers. But this category has tighter inventory and rising competition, especially as more empty nesters list their larger homes before year-end.

- One-to-one swap advice: A market like this favors downsizers who can sell high and buy strategically. You may even benefit from mortgage buydown credits, or shorter contingencies.

I know President Trump hopes that ousting Fed officials accelerates rate cuts, but that approach could stoke market anxiety and higher long-term yields, working against his goal. Homebuyers and sellers should keep a close eye on Fed communications rooted in economic data to anticipate mortgage rate trends.